A Guide to Filing Bankruptcy in Pennsylvania Without an Attorney

The prospect of filing for bankruptcy is daunting, and the added cost of hiring a lawyer can feel like an insurmountable barrier. In Pennsylvania, it is legally permissible to file for bankruptcy on your own, a process known as pro se representation. While this path is complex and carries significant risks, it is a choice many make out of financial necessity. Understanding the meticulous process, the stringent requirements, and the potential pitfalls is essential for anyone considering navigating the Pennsylvania bankruptcy courts without legal counsel. This guide provides a detailed roadmap, but it is crucial to recognize it as informational, not a substitute for legal advice tailored to your unique situation.

Understanding the Bankruptcy Process and Your Options

Before taking any step, you must determine which chapter of bankruptcy is appropriate for your circumstances. For individuals, the two primary options are Chapter 7 and Chapter 13. Chapter 7, often called liquidation, is designed for those with limited income who cannot repay their debts. It involves the sale of non-exempt assets by a court-appointed trustee to pay creditors, after which most remaining unsecured debts are discharged. Pennsylvania has its own set of exemption laws that protect certain property, like a portion of home equity, a vehicle, and personal items. Your income must pass the “means test,” which compares your household income to the Pennsylvania median for a similar family size, to qualify for Chapter 7.

Chapter 13, known as a wage earner’s plan, is for individuals with a regular income who can repay a portion of their debts over time. It involves proposing a three to five year repayment plan to the court. This chapter allows you to keep all your property, including non-exempt assets, but you must make monthly payments to the bankruptcy trustee. Chapter 13 is often used to stop foreclosures by catching up on missed mortgage payments over the life of the plan. Choosing the wrong chapter can lead to your case being dismissed, causing you to lose filing fees and potentially putting your assets at risk. Therefore, thorough research into both chapters is the foundational first step.

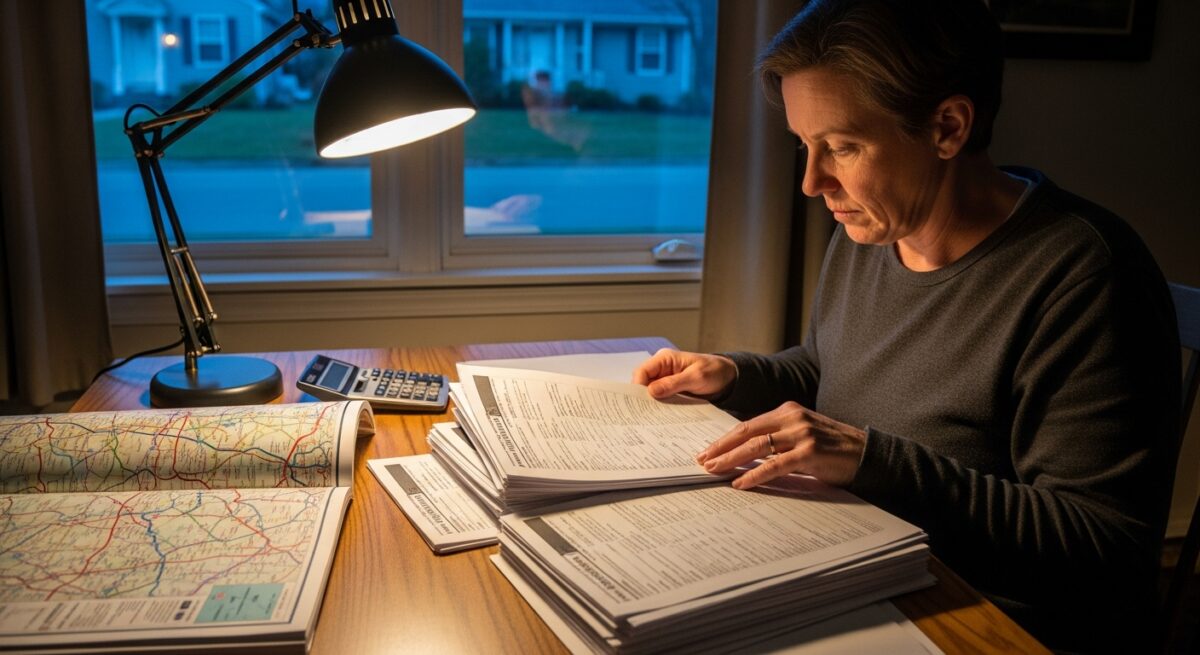

Gathering Documentation and Completing Credit Counseling

The bankruptcy process is document-intensive. You will be required to provide a comprehensive financial snapshot to the court. Gathering these documents before you begin filling out forms will make the process smoother. You will need detailed records of all sources of income, including pay stubs, tax returns, and profit and loss statements if self-employed. A complete list of all creditors, their addresses, and the amounts owed is non-negotiable. You must also document all your assets: real estate deeds, vehicle titles, bank statements, retirement account statements, and a detailed inventory of personal property.

Before you can file your petition, federal law mandates that you complete a credit counseling course from an approved agency. This course must be taken within 180 days before filing. You will receive a certificate of completion, which you must file with your bankruptcy forms. The purpose is to ensure you have explored all possible alternatives to bankruptcy. Failing to file this certificate will result in the dismissal of your case. The United States Courts website provides a list of approved credit counseling agencies for Pennsylvania.

Preparing and Filing the Bankruptcy Petition

This is the most technically demanding part of the pro se process. You must accurately complete a lengthy set of official bankruptcy forms, known as the voluntary petition, schedules, and statements. These forms ask for every detail of your financial life: assets, debts, income, expenses, property claimed as exempt, and recent financial transactions. Errors or omissions can be considered fraud, leading to your case being dismissed or debts not being discharged. All forms must use the correct format for the United States Bankruptcy Court for your district in Pennsylvania (Eastern, Middle, or Western District).

The key forms include the petition itself (Official Form 101), schedules detailing your assets (Form 106A/B) and liabilities (Form 106D), your income (Form 106I) and expenses (Form 106J), and the statement of financial affairs (Form 107). You must also complete the means test calculation (Form 122A-1 for Chapter 7 or Form 122C-1 for Chapter 13). After completing all forms, you must file them with the bankruptcy court clerk in the correct district. This requires paying the filing fee, which is several hundred dollars, though you can apply for a fee waiver or installment plan if you cannot afford it. Upon filing, the automatic stay immediately goes into effect, stopping most collection actions against you.

Navigating the 341 Meeting and Post-Filing Requirements

After filing, you will be assigned a bankruptcy trustee and a date for the meeting of creditors, commonly called the 341 meeting. This is a mandatory hearing where the trustee and any creditors who choose to attend can ask you questions under oath about your finances and the information in your paperwork. While often brief, this meeting is formal and legally binding. You must bring your photo ID, Social Security card, and all the financial documentation you used to prepare your forms. The trustee will verify your identity and ask a series of standard questions. Being unprepared or providing inconsistent answers can have serious consequences.

Following the 341 meeting, you have additional tasks. In a Chapter 7 case, you must cooperate with the trustee if any non-exempt assets need to be liquidated. In a Chapter 13 case, you must begin making your plan payments to the trustee within 30 days of filing, even before your plan is confirmed by the judge. Furthermore, before receiving a discharge, you must complete a second educational course on personal financial management from an approved provider. You must file the certificate for this debtor education course to close your case successfully. For a deeper analysis of court procedures and trustee expectations, Read full article for detailed case reviews.

Common Risks and Challenges of Filing Pro Se

Choosing to file without a lawyer involves accepting substantial risk. The bankruptcy code and rules are exceptionally complex. A simple mistake on a form, such as improperly valuing an asset or omitting a creditor, can lead to that debt not being discharged. You might inadvertently forfeit property you could have protected with proper exemption planning. The trustee and creditors are represented by experienced attorneys, and you will be at a significant disadvantage in any adversarial proceeding. If your case is challenged or becomes contested, you will be responsible for knowing and applying federal and state bankruptcy law, local court rules, and procedural requirements.

Furthermore, certain situations make pro se filing particularly hazardous. These include having significant equity in a home, owning a business, facing lawsuits from creditors, having debts that may be non-dischargeable (like certain taxes or student loans), or having income above the state median. In these scenarios, the cost of an attorney may be an investment that saves you money and property in the long run. Many bankruptcy attorneys offer free initial consultations and flexible payment plans, which are worth exploring before deciding to proceed alone.

Frequently Asked Question

What is the biggest mistake people make when filing bankruptcy without a lawyer in PA?

The most common and critical mistake is failing to properly claim exemptions. Pennsylvania allows filers to choose between federal and state exemption systems, and the choice is irreversible. Selecting the wrong system, or incorrectly listing property under an exemption, can result in losing assets like cash, vehicles, or heirlooms to the trustee. Another major error is transferring or selling property before filing in an attempt to hide it, which is considered fraud and can lead to the denial of your entire discharge.

Can I change from a Chapter 7 to a Chapter 13 case if I filed pro se?

Yes, you can file a motion to convert your case from Chapter 7 to Chapter 13, provided you meet the eligibility requirements for Chapter 13. However, this requires filing additional correct legal motions with the court, and there are strict deadlines. If your Chapter 7 case is near discharge or if assets have already been administered, conversion may not be possible. This procedural complexity highlights why legal guidance is often crucial.

Where can I find the official bankruptcy forms and local rules for Pennsylvania?

All official federal bankruptcy forms are available for free on the United States Courts website. For local rules and specific filing procedures, you must visit the website for your specific Pennsylvania Bankruptcy Court district (Eastern, Middle, or Western). These sites provide crucial information on filing fees, required formats, and local trustee practices.

Filing for bankruptcy in Pennsylvania without an attorney is a rigorous, self-directed legal undertaking. It demands a high level of personal organization, attention to detail, and a willingness to navigate complex federal and state procedures. While it can eliminate qualifying debt, the risks of procedural missteps are real and can undermine the entire effort. For straightforward cases with very few assets, it may be a viable path. However, given the long-term financial and legal consequences, consulting with a qualified Pennsylvania bankruptcy attorney, even for a single review of your prepared documents, is a prudent step that can provide invaluable protection and peace of mind.

About Jason Mitchell

Recent Posts

Emergency Bankruptcy Filing in New York: A Complete Guide

Learn how emergency bankruptcy in New York can immediately stop foreclosures and garnishments. Call (833) 227-7919 for urgent guidance.

Failing Debtor Education in Illinois: Consequences and Solutions

Failing debtor education in Illinois can result in a denied bankruptcy discharge, leaving all debts intact. Protect your fresh start; call (833) 227-7919 for guidance.

Including Utility Bills in Arizona Bankruptcy Explained

Learn if you can include utility bills in Arizona bankruptcy and protect your service. For expert guidance, call (833) 227-7919.