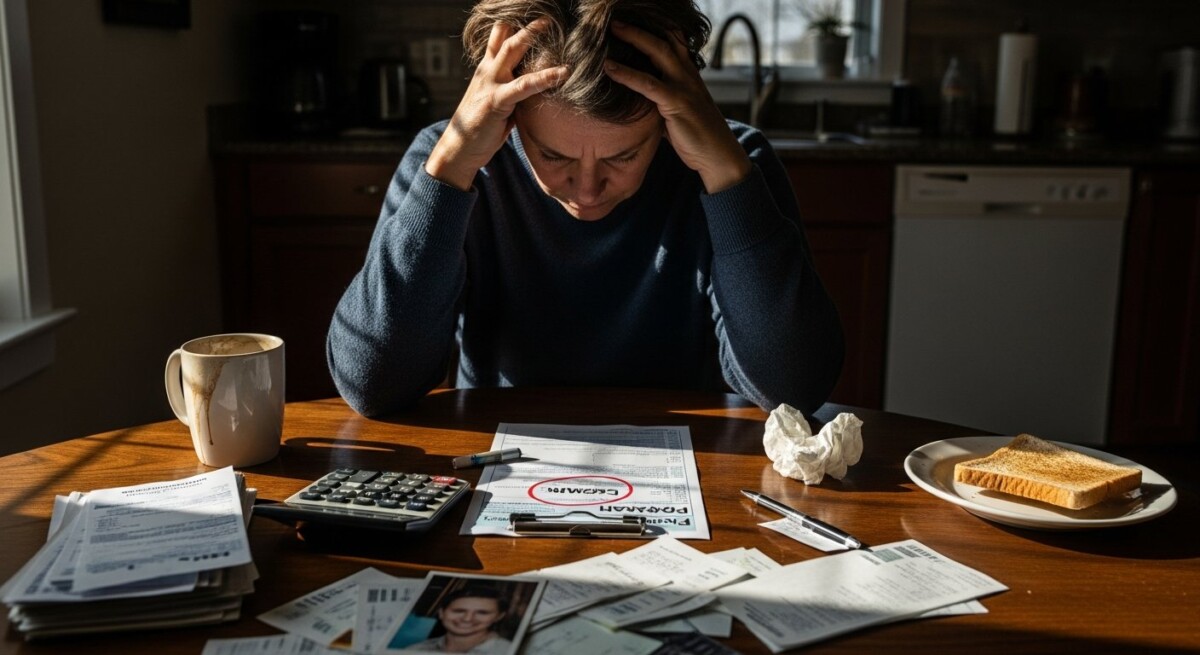

Can You Discharge Payday Loans in Arizona Bankruptcy?

Struggling with the relentless cycle of payday loan debt in Arizona can feel like being trapped in quicksand. Each payday brings not relief, but a scramble to cover the high fees and interest, only to need another loan to make ends meet. For many Arizonans, bankruptcy emerges as a potential path to financial stability. A critical question at the heart of this decision is whether you can include payday loans in bankruptcy in Arizona. The short answer is yes, in the vast majority of cases, payday loans are treated as unsecured debt and can be discharged. However, the process is nuanced, and timing is everything. Understanding how bankruptcy interacts with these high-cost loans is essential for making an informed choice about your financial future.

The Legal Status of Payday Loans in Bankruptcy

Under the U.S. Bankruptcy Code, debts are categorized primarily as secured or unsecured. A secured debt is backed by collateral, like a car loan or mortgage. An unsecured debt has no such collateral. Payday loans, along with credit card debt and medical bills, are almost always classified as unsecured debt. This classification is the first and most important reason why payday loans can be included in bankruptcy. Whether you file for Chapter 7 liquidation or Chapter 13 repayment, these loans are generally eligible for discharge. This means the legal obligation to repay them is erased. However, creditors, especially payday lenders, may attempt to challenge the discharge under certain circumstances, making it crucial to file correctly and with proper legal guidance.

Navigating the 70-Day Rule and Fraud Concerns

The primary hurdle in discharging a payday loan is not its type, but its timing. The bankruptcy code contains a presumption of fraud for certain consumer debts incurred shortly before filing. Specifically, if you take out a payday loan (or any cash advance) of $1,000 or more for “luxury goods or services” within 70 days of filing, the debt is presumed to be nondischargeable. Similarly, if you obtain a cash advance of $1,000 or more under an open-ended credit plan (like a payday loan line of credit) within 70 days of filing, the same presumption applies. The key term here is “presumed.” This does not mean the debt is automatically excluded. It means the creditor has grounds to object, and you would need to demonstrate to the court that you took the loan in good faith, with the intent to repay, and not with the intent to file for bankruptcy immediately afterward. For example, if you took a $1,500 payday loan 50 days before filing to cover an emergency car repair so you could get to work, you could argue good faith. If you took the same loan for a luxury vacation, your argument weakens considerably. This is a complex area where the advice of a skilled attorney is invaluable. A professional can help you time your filing and build a strong case for your intent, a process detailed in resources like how an Arizona bankruptcy lawyer can secure your financial future.

Chapter 7 vs. Chapter 13: Two Paths for Payday Loan Debt

The type of bankruptcy you file significantly impacts how your payday loan debt is handled. In a Chapter 7 bankruptcy, your non-exempt assets are liquidated by a trustee to pay creditors a portion of what is owed. Most unsecured debts, including payday loans, are then discharged, meaning you owe nothing further. Most Arizona filers qualify for Chapter 7 under the means test, and if their payday loans fall outside the problematic 70-day window, these debts are typically wiped away cleanly. Chapter 13 bankruptcy, on the other hand, involves a court-approved repayment plan lasting three to five years. You repay a portion of your debts through the plan based on your disposable income. Here, payday loans are included in the pool of unsecured debts. They are often paid only a small percentage of what is owed, sometimes even zero percent, with the remaining balance discharged at the end of the successful plan. Chapter 13 can be particularly powerful for those with assets they wish to protect, such as a home with significant equity. For homeowners, understanding keeping your Arizona home in Chapter 13 bankruptcy is a critical part of the planning process.

Automatic Stay: Immediate Relief from Collection

One of the most immediate benefits of filing for bankruptcy, under either chapter, is the automatic stay. This is a court order that goes into effect the moment your petition is filed. It legally prohibits creditors from any collection activity. For someone besieged by payday lenders, this means:

- All collection calls and letters must stop immediately.

- Any pending wage garnishment must cease.

- Lawsuits filed by the lender are put on hold.

- Threats of repossession or bank account levies are halted.

This breathing room is often the first step toward regaining control of your financial life. The automatic stay provides a shield while your bankruptcy case proceeds, allowing you to work with your attorney without the constant pressure of aggressive collection tactics.

Steps to Successfully Include Payday Loans in Your Filing

To ensure your payday loans are properly handled in bankruptcy, a methodical approach is required. Rushing the process can lead to objections or allegations of fraud. Follow these key steps:

- Cease Borrowing: Stop taking out any new payday loans or cash advances immediately. Continuing to borrow after deciding to file can be seen as bad faith.

- Gather Documentation: Collect all loan agreements, statements, bank records showing deposits and withdrawals, and records of any rollovers or payments made. This creates a clear paper trail.

- Consult a Bankruptcy Attorney: This is the most critical step. An attorney will analyze the timing of your loans, assess your overall financial picture, and determine the best chapter for you to file under. They will ensure all debts are listed correctly on your petition.

- Plan Your Filing Date: With your attorney, decide on an optimal filing date. If you have recent large payday loans, it may be advisable to wait until the 70-day presumption period passes to avoid an objection, unless you have a strong good-faith argument.

- List All Lenders Accurately: Your attorney will ensure every payday lender is listed with their correct legal name and address on your bankruptcy schedules. This is necessary for them to receive formal notice and for the debt to be discharged.

Following these steps with professional help dramatically increases the likelihood of a smooth process. For a broader view of this journey, consider navigating financial relief with a bankruptcy lawyer in Arizona.

Frequently Asked Questions

What if the payday lender has a post-dated check or access to my bank account? The automatic stay prevents them from cashing the check or making an electronic withdrawal. You must list them as a creditor, and you should also formally revoke the ACH authorization with your bank in writing, providing a copy of your bankruptcy filing notice.

Can a payday loan be reaffirmed? While possible, reaffirming a payday loan (agreeing to keep paying it after bankruptcy) is almost never advisable. It defeats the purpose of seeking debt relief and binds you to a high-cost contract you are trying to escape.

What happens if I forgot to list a payday loan? You can amend your schedules to add the omitted creditor. It is important to do this as soon as you realize the mistake, as an unlisted debt may not be discharged.

Are online payday loans treated differently? No. Legally, they are the same as storefront loans. The key is identifying the actual lending company to list on your bankruptcy paperwork, which can sometimes be challenging with online entities.

Will including payday loans affect my bankruptcy case negatively? Not inherently. The court is accustomed to seeing these debts. The issue arises only with recent large loans, where timing and intent become relevant factors that your attorney can address.

Successfully navigating bankruptcy with payday loan debt requires careful strategy and a clear understanding of both state and federal law. The principles of proper timing and full disclosure, as emphasized in resources like how a Charlotte bankruptcy lawyer can secure your financial future, apply universally. While the process may seem daunting, the goal is a fresh financial start, free from the crushing cycle of high-interest debt. By taking informed, deliberate steps with professional counsel, you can use the bankruptcy system as it is intended: as a legal tool to achieve solvency and peace of mind.

About Talia Rosen

Recent Posts

How Long Does a Chapter 7 Trustee Take to Close a Case in Georgia?

Understand the timeline for a Chapter 7 trustee to close a case in Georgia. For expert guidance, call (833) 227-7919.

What Happens When Your Mortgage Lender Contests Bankruptcy in Florida?

If your mortgage lender contests bankruptcy in Florida, know your rights and options. Call (833) 227-7919 for a consultation to protect your home.

Negotiate With Creditors Before Filing Bankruptcy in California

Learn if you can negotiate with creditors before filing in California to potentially avoid bankruptcy. Call (833) 227-7919 for a confidential consultation.